The Dual Challenge: Integrating into Delegate and Machine Economies in Agentic Payments

What Every Business Leader and Financial Professional Needs to Know

As agentic rails reshape the payments landscape, business leaders and financial services professionals face a pivotal question: How will you integrate into both the Delegate Economy - where agents act on behalf of humans within legacy financial systems and the Machine Economy, where autonomous agents transact natively with wallets and tokenized money? Preparing for both models is essential, as the interplay between human delegation and machine-to-machine transactions will define the future of commerce.

Something shifted in the past few weeks. Not incrementally. Structurally. Foundational infrastructure for the Agentic economy has been shipped. More primitives have been added to Agentic tech stacks. And the tension around standards for the Delegate and Machine Economy is rising.

In March and early April, Stripe, Visa, J.P. Morgan and Coinbase shipped foundational infrastructure and primitives for the Agentic economy.

In March, Stripe and Tempo launched the Machine Payments Protocol (MPP), an open standard for agent-initiated payments. Visa extended it to card rails on day one, in their effort to remain relevant. At launch, more than 100 services were listed as integrations, including Anthropic, OpenAI, Shopify, and DoorDash. By now, both Visa and Mastercard have extended their payment rails to support agent-initiated transactions via MPP. The first major incumbent bank to also integrate is Standard Chartered, which means it can custody funds, verify agent identity, and provide compliance for agent-initiated transactions. The first two digital-first banks to integrate – surprise, surprise - are Revolut and Nubank, which means their customers and their own internal systems will be able to leverage agent-initiated payments for things like automated bill pay, instant transfers, and other programmable financial services. The first large Fintech to integrate is Ramp, the expense management and corporate cards scale-up, which means they are looking to enable autonomous agents to manage expenses, pay invoices, and optimize spending through Agents.

In early April, Visa moved beyond “support” to orchestration by unveiling Intelligent Commerce Connect. A single integration layer for secure agent payment initiation, tokenization, spend controls, authentication, and even merchant-catalog discoverability. This is built to work across Visa and non‑Visa rails and to accept transactions initiated via major agent protocols (including MPP and UCP).

In early March, J.P. Morgan partnered with Mirakl, a leading provider of enterprise marketplace infrastructure whose platform powers online marketplaces for major retailers and manufacturers globally. Together, they are building an agentic checkout layer that enables tokenized, agent-initiated transactions with bank-grade fraud protection. This solution is designed for merchants operating on Mirakl’s platform and those using J.P. Morgan Payments, making agentic commerce accessible to enterprise clients who want secure, scalable automation without building their own integrations.

As a payment giant, J.P. Morgan is bringing trusted financial rails and risk management to the agentic commerce space. Unlike open agentic rails such as Tempo and orchestration layers from Visa, which aim to create broad, interoperable standards for agent-driven payments, the J.P. Morgan and Mirakl approach focuses on delivering integrated infrastructure for enterprise marketplaces. Their solution combines intelligent commerce discovery, secure payments, fraud protection, and governance, positioning it as a full-stack offering for large merchants. J.P. Morgan is clear that the differentiator in this space will not be AI alone, but robust governance and risk management.

During the same period, Coinbase went all-in. They shipped Agentic Wallets for AI agents and, in April, launched Agentic.Market as a discovery layer for agent services built on x402. Brian Armstrong made the structural point clear: traditional corporate cards cannot be issued to non-human entities. Stablecoin wallets for agents are the answer.

This marks a fundamentally different approach from the agentic rails and orchestration layers being built by Tempo, J.P. Morgan, and the card networks. While those players are adapting their existing infrastructure to support agent-driven payments - often within closed or semi-open ecosystems - Coinbase is betting on open protocols, self-custody, and direct agent control. The competition is now underway: will the future of agentic commerce be shaped by open, programmable standards and self-custody wallets, or by the trusted rails and governance of established financial giants?

In addition, the x402 rails found a neutral home when the Linux Foundation launched the x402 Foundation and accepted Coinbase’s contribution of the x402 protocol, explicitly positioning it as an open, vendor-neutral standard for payments over HTTP.

The launch of the x402 Foundation under the Linux Foundation brought together a coalition of traditional payment networks, cloud providers, fintechs, and commerce platforms - including Visa, Mastercard, Stripe, Google, AWS, and Shopify[1]. Their participation signals that the industry is hedging its bets, supporting both proprietary agentic rails and open, vendor-neutral protocols. As agentic commerce evolves, these players are positioning themselves to remain relevant in whichever scenario - closed or open - ultimately prevails.

As agentic rails mature, another foundational question emerges: how do we establish trust and identity for autonomous agents operating across these networks?

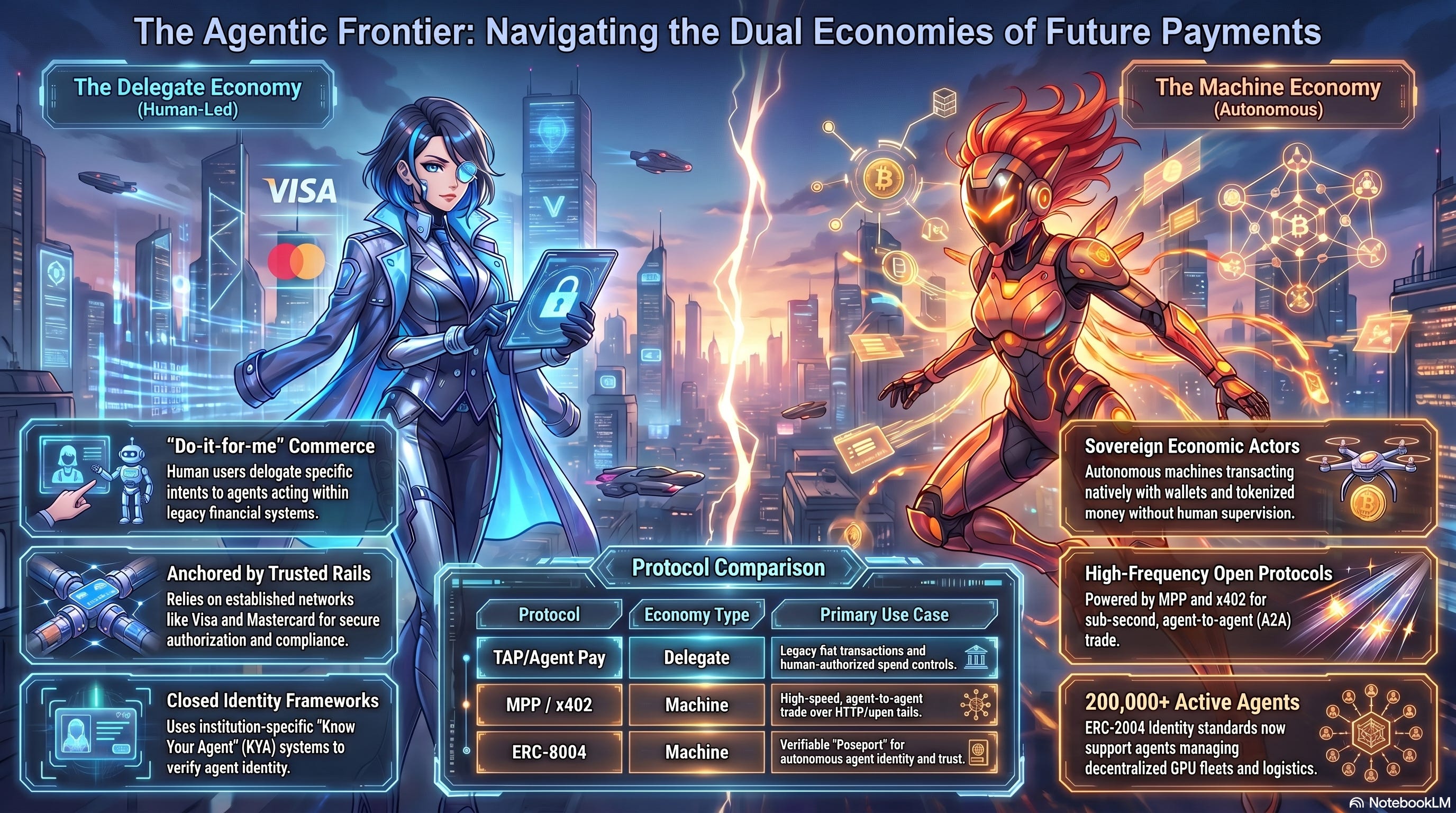

As agentic rails evolve, the question of agent identity becomes central. ERC-8004, an Ethereum standard for agent identity, provides a verifiable, interoperable passport for autonomous agents. This standard is being adopted by platforms like Base and protocols like x402, enabling agents to transact securely and seamlessly across open payment networks. By integrating ERC-8004, Coinbase and Base are positioning themselves at the intersection of open payments and open identity, in contrast to proprietary rails that rely on closed identity systems. Including ERC-8004 in the agentic rails stack signals a shift toward programmable, compliant, and scalable agent-driven commerce.

In 2026, the use of the ERC-8004 standard surged from a few hundred agents to 200,000+ agents. The important shift is from agents foccused on DeFi yield-farming and on-chain gaming, to Agents autonomously managing decentralized GPU fleets and brokering complex enterprise logistics without human oversight. These currently account for more than 50% of active agent profiles.

The convergence of open payment protocols and open identity standards marks a new chapter for agentic commerce - one where software agents can transact, identify themselves, and build trust across the global economy.

While ERC-8004 offers an open, interoperable standard for agent identity, many proprietary agentic rails - including Visa’s Trusted Agent Protocol, Mastercard’s Agent Pay, MetaComp’s StableX KYA Framework, and Trulioo’s Digital Agent Passport - rely on closed or institution-specific Know Your Agent frameworks. These approaches typically require agents to be registered, verified, and managed within the boundaries of a particular platform or financial institution, often limiting interoperability and programmability across networks. By contrast, ERC-8004 enables agents to carry a verifiable, portable identity that works across open payment protocols like x402 and platforms such as Base, supporting seamless transactions and compliance in a decentralized environment.

A notable example of a proprietary approach is American Express, which is piloting agent-driven payment frameworks through its Agentic Commerce Engine (ACE) within its closed-loop network. This model remains exclusive to the AMEX ecosystem, contrasting with the open and interoperable rails being developed by Visa, Mastercard, Stripe/Tempo, and x402.

Where This Leaves Us

As agentic commerce matures, the choice between open identity standards and proprietary KYB/KYA frameworks will shape not only how agents transact, but also who controls the future of autonomous economic activity.

As this infrastructure matures, it is becoming clear that activity in agentic rails is separating into two distinct, yet interconnected, economic buckets. The Delegate Economy is the realm of “Do-it-for-me” commerce, where humans delegate specific intents to agents. Protocols like Visa’s Trusted Agent Protocol (TAP), Mastercard’s Agent Pay, and the Agentic Commerce Protocol (ACP) thrive here. These systems focus on secure authorization, spend controls, and Know Your Agent (KYA) frameworks that allow humans to trust software with their legacy financial credentials, preserving the fiat world for agent-driven transactions.

The Machine Economy, by contrast, is an entirely new category, one where machines act as sovereign economic actors, transacting without direct human supervision. This is where the Machine Payments Protocol (MPP) developed by Stripe and Tempo, and the Linux Foundation’s x402 protocol provide high-frequency, sub-second settlement rails for agent-to-agent (A2A) trade. Here, agents operate natively with wallets and tokenized money, leveraging open identity standards like ERC-8004 to transact across decentralized networks.

While established giants like J.P. Morgan and Visa are leveraging their trusted rails to lead the Delegate Economy, Coinbase and the ERC-8004 standard are building the “passport” and “wallet” for the sovereign Machine Economy.

Ultimately, the industry is hedging its bets. The winner will not just be the one with the fastest AI, but the one that provides the most robust governance for a world where software is the primary engine of global transaction volume.

For business leaders and financial services professionals, the imperative is clear: readiness for both the Delegate Economy and the Machine Economy is not optional. Whether your organization leverages trusted rails to preserve fiat-based agentic transactions or embraces open protocols and tokenized money for autonomous, machine-to-machine commerce, strategic integration into both worlds will determine your relevance and resilience in the evolving agentic landscape.

Leading organizations - including Standard Chartered, JP Morgan, Stripe, Revolut, Nubank, Adyen, Circle, and Ramp - are already positioning themselves for this dual future.

The Agentic Economy Meets the Tokenized World.

Dr. Efi Pylarinou

Top Global Fintech and Tech Thought Leader

Publisher, Weekly Agentic AI for Financial Services Newsletter

[1] The x402 Foundation’s founding and early members include also Cloudflare, Microsoft, Visa, Mastercard, American Express, Adyen, Circle, Shopify, Solana Foundation, Polygon Labs, PPRO, Fiserv Merchant Solutions, KakaoPay, Base, thirdweb, Merit Systems, and Sierra.

The "delegate economy" framing here is a useful lens that most technical writing about x402 misses. Business leaders and financial professionals aren't asking how the HTTP 402 status code works. They're asking: when my AI agent spends money on my behalf, what are my controls, my audit trails, and my liability exposure? Those are legitimate questions that the current x402 implementation doesn't fully answer at the enterprise level. The dual challenge is real: you have to integrate into the machine economy (agents paying agents via x402 and similar protocols) while simultaneously maintaining trust and accountability in the delegate economy (humans authorizing agents to act on their behalf). The compliance layer between those two is still being designed. Traditional businesses that start deploying agentic workflows without solving the governance and reporting layer first will create audit nightmares. The financial professionals reading this post should focus less on the crypto mechanics and more on the spending policy architecture they need to have in place before agents start transacting.